Before you get life insurance coverage, you should understand why you need it. While there are many reasons to buy life insurance, the most common reasons include:

Final expenses: Final expenses refer to any expenses related to someone’s passing. This can include a casket, funeral, preparations, memorial service, cremation and more. Life insurance for final expenses is worth considering—after all, the National Funeral Directors Association reports that the median price of a funeral with a casket is around $7,850. Families without enough funds are forced to cut back on the service or ask friends and family for donations. Some families have turned to crowdfunding to help cover the cost. A modest term life insurance policy can unburden your loved ones by taking care of these expenses.

Income replacement: Your loved ones depend on your income to meet daily needs for food, medical care, utilities, car payments and much more. There are also future costs like a child’s college education or contributions you would have made toward a surviving spouse’s retirement.… Read More

Before you get life insurance coverage, you should understand why you need it. While there are many reasons to buy life insurance, the most common reasons include:

Final expenses: Final expenses refer to any expenses related to someone’s passing. This can include a casket, funeral, preparations, memorial service, cremation and more. Life insurance for final expenses is worth considering—after all, the National Funeral Directors Association reports that the median price of a funeral with a casket is around $7,850. Families without enough funds are forced to cut back on the service or ask friends and family for donations. Some families have turned to crowdfunding to help cover the cost. A modest term life insurance policy can unburden your loved ones by taking care of these expenses.

Income replacement: Your loved ones depend on your income to meet daily needs for food, medical care, utilities, car payments and much more. There are also future costs like a child’s college education or contributions you would have made toward a surviving spouse’s retirement.… Read More

Top Three Reasons Why People Buy Life Insurance

Before you get life insurance coverage, you should understand why you need it. While there are many reasons to buy life insurance, the most common reasons include:

Final expenses: Final expenses refer to any expenses related to someone’s passing. This can include a casket, funeral, preparations, memorial service, cremation and more. Life insurance for final expenses is worth considering—after all, the National Funeral Directors Association reports that the median price of a funeral with a casket is around $7,850. Families without enough funds are forced to cut back on the service or ask friends and family for donations. Some families have turned to crowdfunding to help cover the cost. A modest term life insurance policy can unburden your loved ones by taking care of these expenses.

Income replacement: Your loved ones depend on your income to meet daily needs for food, medical care, utilities, car payments and much more. There are also future costs like a child’s college education or contributions you would have made toward a surviving spouse’s retirement.… Read More

They say that the only constant in life is change. And that’s true whether you’re 18, 80 or somewhere in between.

One thing to consider when life changes is your insurance coverage. Here are six common transitions that we can help you navigate.

You’re off to college.

With many policies, full-time students younger than 24 are automatically covered under their parents’ homeowners policy. Part-time students (or students who are 24 and older) may need to take out a renters insurance policy. If you choose to live in an apartment instead of a dorm, think about purchasing a separate renters insurance policy. (Learn more about renters insurance below.) When it comes to car insurance, you don’t need your own policy if you’re taking a family member’s car to school. If you’re a co-owner on the vehicle or if you own your own car, you probably need your own policy.

You’re renting your first place.…

They say that the only constant in life is change. And that’s true whether you’re 18, 80 or somewhere in between.

One thing to consider when life changes is your insurance coverage. Here are six common transitions that we can help you navigate.

You’re off to college.

With many policies, full-time students younger than 24 are automatically covered under their parents’ homeowners policy. Part-time students (or students who are 24 and older) may need to take out a renters insurance policy. If you choose to live in an apartment instead of a dorm, think about purchasing a separate renters insurance policy. (Learn more about renters insurance below.) When it comes to car insurance, you don’t need your own policy if you’re taking a family member’s car to school. If you’re a co-owner on the vehicle or if you own your own car, you probably need your own policy.

You’re renting your first place.…  Have you ever read the children’s book Love You Forever, where the mother cares for her growing son until, as a grown man, the son cares for his aging mother? The story depicts a parent/child role reversal that many experience in real life.

Talking about aging with parents can be difficult. But being honest about the topic is important. To help guide the conversation, here are four common concerns you may face with an aging parent and tips on how to address them.

Decide on Living Arrangements Early

Multi-level homes or complicated floor plans might make everyday living difficult and dangerous for aging parents. Discussing it sooner rather than later, while parents are active and not in a distressed state, can help them ease into the idea of new living arrangements like a one-story home or assisted living facility.

If parents insist on staying in their current home, consider homecare and installing assistive equipment, like handrails, as needed.…

Have you ever read the children’s book Love You Forever, where the mother cares for her growing son until, as a grown man, the son cares for his aging mother? The story depicts a parent/child role reversal that many experience in real life.

Talking about aging with parents can be difficult. But being honest about the topic is important. To help guide the conversation, here are four common concerns you may face with an aging parent and tips on how to address them.

Decide on Living Arrangements Early

Multi-level homes or complicated floor plans might make everyday living difficult and dangerous for aging parents. Discussing it sooner rather than later, while parents are active and not in a distressed state, can help them ease into the idea of new living arrangements like a one-story home or assisted living facility.

If parents insist on staying in their current home, consider homecare and installing assistive equipment, like handrails, as needed.…  In the vast majority of cases, you won’t get a payout when your term life insurance policy expires. The exception is a return of premium policy, which returns all of the money you paid over the years back to you. However, the premium is usually much higher for this option than it would be for the average term life policy.

To avoid losing the premiums you’ve paid out over the years, you might consider converting your term life policy to a permanent policy like whole life or universal life. For many, life and financial circumstances might have made a term life policy the best choice in the past. Now might be the right time to change to a permanent policy.

The differences between a term life and permanent life policy

A term life policy tends to be more affordable, but only covers you for a specific amount of time. Policy lengths can last from as little as five years to as long as 30 years.…

In the vast majority of cases, you won’t get a payout when your term life insurance policy expires. The exception is a return of premium policy, which returns all of the money you paid over the years back to you. However, the premium is usually much higher for this option than it would be for the average term life policy.

To avoid losing the premiums you’ve paid out over the years, you might consider converting your term life policy to a permanent policy like whole life or universal life. For many, life and financial circumstances might have made a term life policy the best choice in the past. Now might be the right time to change to a permanent policy.

The differences between a term life and permanent life policy

A term life policy tends to be more affordable, but only covers you for a specific amount of time. Policy lengths can last from as little as five years to as long as 30 years.…  Do you know how much it takes to raise a child these days? Are you sitting down?That would be almost a quarter of a million dollars. It costs $245,000 to raise a child born in 2013 until they hit 18, according to the

Do you know how much it takes to raise a child these days? Are you sitting down?That would be almost a quarter of a million dollars. It costs $245,000 to raise a child born in 2013 until they hit 18, according to the

As a young insurance agent, Mark Wandall didn’t needed to be convinced to buy life insurance. But even Mark would be amazed at all that the insurance has meant for his wife, Melissa, and for many other people he never met.

Mark was just 30 when he was killed in an auto accident less than a mile from his Bradenton, Florida, home. He was the passenger in a car that was broadsided by a driver who ran a

As a young insurance agent, Mark Wandall didn’t needed to be convinced to buy life insurance. But even Mark would be amazed at all that the insurance has meant for his wife, Melissa, and for many other people he never met.

Mark was just 30 when he was killed in an auto accident less than a mile from his Bradenton, Florida, home. He was the passenger in a car that was broadsided by a driver who ran a  Quick quiz: Who needs life insurance the most?

A married 25-year-old who just bought a house

A 38-year-old homeowner with three children

A 59-year-old nearing retirement and caring for an

aging parent

The answer: All of the above.

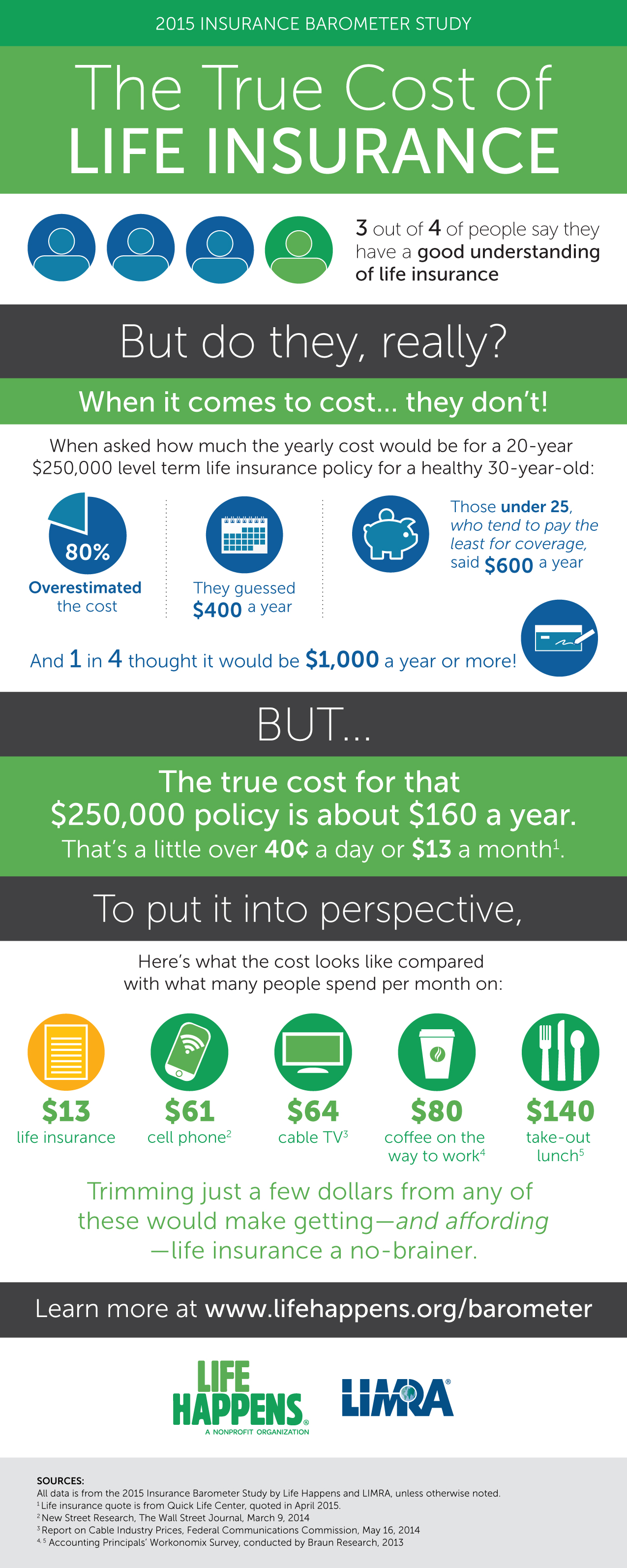

Surprised? You’re not alone in underestimating the role that life insurance plays in protecting loved ones and in ensuring a comfortable retirement. Or in overestimating its cost: A recent study reveals that consumers think life insurance is

Quick quiz: Who needs life insurance the most?

A married 25-year-old who just bought a house

A 38-year-old homeowner with three children

A 59-year-old nearing retirement and caring for an

aging parent

The answer: All of the above.

Surprised? You’re not alone in underestimating the role that life insurance plays in protecting loved ones and in ensuring a comfortable retirement. Or in overestimating its cost: A recent study reveals that consumers think life insurance is